Buying your first home is one of the biggest financial decisions you’ll ever make. Whether you’re purchasing a cozy apartment, a suburban house, or your dream family home, understanding the true cost of a mortgage is critical before signing any loan agreement.

This is where a home loan calculator becomes one of the most valuable tools in your home-buying journey.

Many first-time buyers focus only on the property’s price and forget to calculate the long-term impact of interest rates, loan tenure, down payments, and monthly repayments. A home loan calculator helps eliminate guesswork by providing a realistic picture of what you’ll pay over the life of the loan.

In this comprehensive guide, we’ll explain how home loan calculators work, why they matter, how to use them effectively, and how they can help you make smarter financial decisions before committing to a mortgage.

What Is a Home Loan Calculator?

A home loan calculator is an online financial tool designed to estimate your monthly mortgage payments based on key loan details.

Typically, the calculator requires:

- Loan amount

- Interest rate

- Loan tenure (repayment period)

- Down payment (optional)

- Property value (optional)

Using these inputs, it calculates:

- Monthly EMI (Equated Monthly Installment)

- Total interest payable

- Total repayment amount

- Amortization schedule

- Principal vs. interest breakdown

Instead of manually performing complex financial calculations, the calculator instantly generates accurate estimates, helping buyers evaluate affordability before applying for a loan.

Why First-Time Home Buyers Need a Home Loan Calculator

Many people apply for a mortgage based solely on the maximum amount a lender is willing to offer.

This can be a costly mistake.

Just because a bank approves a large loan doesn’t necessarily mean it fits comfortably within your budget.

A home loan calculator helps you:

Understand Your Monthly Commitment

Knowing your monthly EMI beforehand prevents financial surprises after purchasing the property.

Compare Different Loan Options

You can quickly test various:

- Loan amounts

- Interest rates

- Repayment periods

This allows you to identify the most affordable option.

Plan Your Budget

Homeownership involves more than mortgage payments.

You’ll also need to budget for:

- Property taxes

- Home insurance

- Maintenance costs

- Utility bills

- Repairs

- Homeowners association fees

A calculator helps ensure your mortgage remains manageable alongside these expenses.

Reduce Financial Stress

When you know exactly what to expect, you’re less likely to overextend yourself financially.

How a Home Loan Calculator Works

Most calculators use a standard EMI formula to determine monthly payments.

The calculation considers:

- Principal loan amount

- Monthly interest rate

- Total repayment period

The relationship between these variables determines how much you’ll pay every month.

The higher the:

- Loan amount

- Interest rate

- Loan duration

…the more you’ll pay overall.

However, longer loan tenures typically reduce monthly payments while increasing total interest costs.

EMI Formula Explained

A standard home loan EMI calculation is based on:

EMI=(1+R)N−1P×R×(1+R)N

Where:

- P = Principal loan amount

- R = Monthly interest rate

- N = Number of monthly installments

Fortunately, modern calculators perform these calculations automatically, allowing users to focus on decision-making rather than mathematics.

Key Inputs in a Home Loan Calculator

Understanding each input helps you use the calculator more effectively.

1. Property Price

The total cost of the home you intend to purchase.

Example:

- Property value: $400,000

2. Down Payment

The amount you pay upfront.

Example:

- Property price: $400,000

- Down payment: $80,000 (20%)

Loan amount becomes:

- $320,000

A larger down payment generally means:

- Lower EMI

- Less interest paid

- Better loan approval chances

3. Loan Amount

This is the amount borrowed from the lender.

Formula:

Loan Amount = Property Price − Down Payment

4. Interest Rate

The annual percentage charged by the lender.

Even a small difference matters significantly.

For example:

- 6.5% interest

- 7.5% interest

may result in thousands of dollars of difference over the life of the mortgage.

5. Loan Tenure

Repayment duration.

Common loan terms include:

- 10 years

- 15 years

- 20 years

- 25 years

- 30 years

Longer terms:

✔ Lower monthly payments

But:

✘ Higher total interest costs

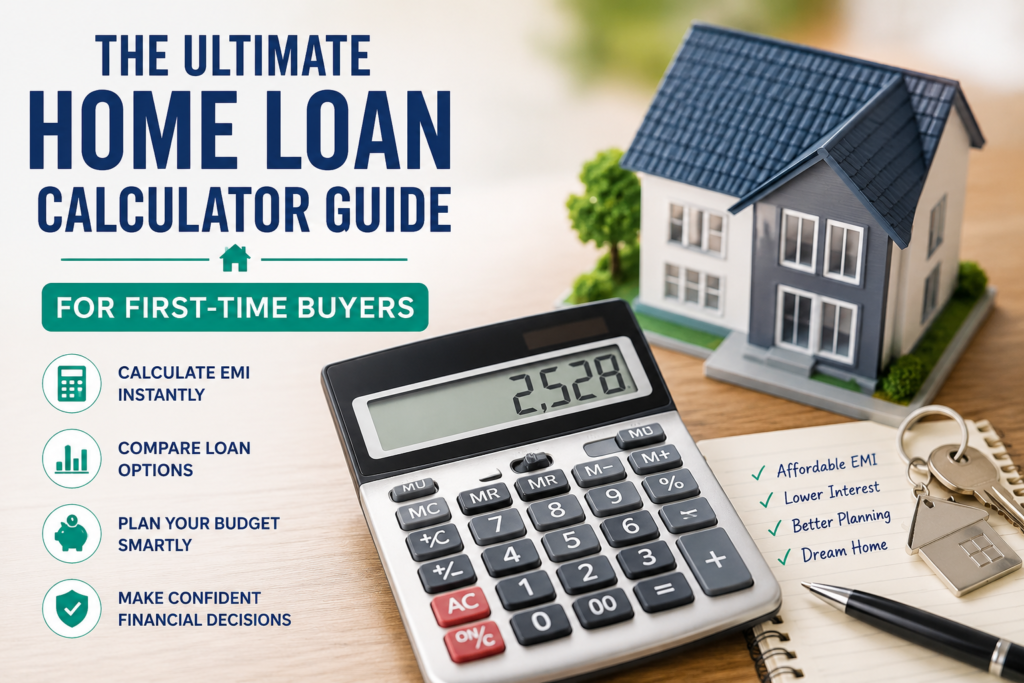

Example Home Loan Calculation

Let’s assume:

| Loan Details | Value |

|---|---|

| Property Price | $500,000 |

| Down Payment | $100,000 |

| Loan Amount | $400,000 |

| Interest Rate | 6.5% |

| Loan Term | 30 Years |

A calculator may estimate:

| Result | Amount |

|---|---|

| Monthly EMI | $2,528 |

| Total Interest | $510,000+ |

| Total Repayment | $910,000+ |

This example highlights an important lesson:

Interest can sometimes exceed the original loan amount over long repayment periods.

Benefits of Using a Home Loan Calculator

1. Instant Financial Clarity

Instead of guessing, you receive immediate estimates based on real numbers.

2. Better Loan Comparisons

Compare multiple scenarios:

| Loan Option | EMI |

|---|---|

| 20-Year Loan | Higher |

| 30-Year Loan | Lower |

| Lower Interest Rate | Lower EMI |

| Higher Down Payment | Lower EMI |

This flexibility helps identify the best option for your financial situation.

3. Avoid Overborrowing

Many first-time buyers become “house rich but cash poor.”

A calculator helps maintain balance between:

- Housing costs

- Savings

- Investments

- Lifestyle expenses

4. Improved Loan Negotiations

Knowing the impact of interest rates gives you leverage when discussing loan terms with lenders.

Even a small rate reduction can save substantial money.

5. Long-Term Financial Planning

The tool allows you to:

- Forecast future payments

- Plan prepayments

- Understand interest obligations

- Prepare for refinancing opportunities

Understanding Amortization Schedules

Most advanced calculators provide an amortization schedule.

This shows:

- Monthly payments

- Principal repayment

- Interest repayment

- Remaining balance

A surprising fact for many first-time buyers:

During the early years of a mortgage, a significant portion of each payment goes toward interest rather than principal.

Example:

| Year | Interest Portion | Principal Portion |

|---|---|---|

| 1 | High | Low |

| 10 | Moderate | Moderate |

| 25 | Low | High |

Understanding this helps borrowers make smarter prepayment decisions.

How Interest Rates Affect Your Mortgage

Interest rates have a dramatic impact on affordability.

Consider a $350,000 loan over 30 years:

| Interest Rate | Approximate EMI |

|---|---|

| 5% | Lower |

| 6% | Higher |

| 7% | Much Higher |

| 8% | Significantly Higher |

Even a 1% increase can add tens of thousands of dollars to the total repayment amount.

This is why comparing lenders is essential.

Fixed vs. Variable Interest Rates

Many home loan calculators allow you to evaluate both options.

Fixed Rate Loans

Advantages:

- Predictable payments

- Easier budgeting

- Protection against rising rates

Disadvantages:

- Often start slightly higher

Variable Rate Loans

Advantages:

- Lower initial rates

- Potential savings if rates fall

Disadvantages:

- Payment uncertainty

- Exposure to market fluctuations

Running both scenarios through a calculator helps determine which aligns with your risk tolerance.

How Extra Payments Save Money

One of the most powerful uses of a home loan calculator is testing additional repayments.

Example:

Monthly EMI: $2,000

Additional monthly payment: $200

Potential benefits:

- Loan paid off years earlier

- Significant interest savings

- Faster equity growth

Many borrowers underestimate the impact of consistent small prepayments.

Common Mistakes First-Time Buyers Make

Ignoring Additional Costs

A mortgage isn’t the only housing expense.

Remember:

- Taxes

- Insurance

- Repairs

- Maintenance

- Legal fees

- Closing costs

Choosing the Longest Loan Automatically

A 30-year loan may seem attractive because of lower monthly payments.

However:

You may pay substantially more interest compared to a 15-year or 20-year mortgage.

Not Comparing Multiple Lenders

Different lenders offer:

- Different interest rates

- Processing fees

- Loan terms

Even small differences matter.

Borrowing the Maximum Approved Amount

Approval does not equal affordability.

Always calculate payments based on your actual budget.

Tips for Using a Home Loan Calculator Effectively

Use Realistic Interest Rates

Don’t rely on promotional rates alone.

Use rates you are likely to qualify for.

Test Multiple Scenarios

Try:

- Different down payments

- Different loan tenures

- Different interest rates

Include Future Goals

Consider:

- Family planning

- Career changes

- Investments

- Emergency savings

Recalculate Regularly

As market rates change, revisit your calculations.

How Much House Can You Afford?

Financial experts often recommend that housing costs remain within a reasonable portion of monthly income.

A home loan calculator helps answer questions such as:

- Can I afford this property?

- What loan amount fits my budget?

- How much should I put down?

- What happens if rates increase?

These insights are invaluable for first-time buyers.

Features to Look for in a Modern Home Loan Calculator

The best calculators include:

✔ EMI calculation

✔ Amortization schedules

✔ Extra payment analysis

✔ Interest comparison tools

✔ Loan affordability estimates

✔ Refinancing calculations

✔ Mobile-friendly design

✔ Real-time updates

Advanced tools provide a much deeper understanding than simple EMI calculators.

Final Thoughts

For first-time home buyers, knowledge is just as important as financing.

A home loan calculator transforms complicated mortgage numbers into clear, actionable insights. Instead of relying on estimates or lender marketing materials, you gain a realistic understanding of monthly payments, long-term interest costs, and overall affordability.

Before committing to any mortgage, spend time experimenting with different loan scenarios. Adjust down payments, compare interest rates, and evaluate repayment periods. A few minutes with a home loan calculator can potentially save thousands of dollars over the life of your loan.

Buying a home is a major milestone. Using the right financial tools ensures that milestone becomes a source of stability and wealth—not financial stress.