Money plays a crucial role in almost every aspect of life. Whether you’re paying bills, saving for a vacation, buying a home, or planning for retirement, your financial decisions shape your future. Yet many people struggle with managing their finances simply because they were never taught how.

The good news is that personal budgeting and financial planning are skills anyone can learn. You don’t need to be a financial expert, earn a high income, or spend hours studying complicated investment strategies. With a basic understanding of budgeting principles and a clear financial plan, you can gain control of your money and work toward your financial goals with confidence.

This beginner-friendly guide will walk you through the essentials of personal budgeting and financial planning, helping you create a strong foundation for long-term financial success.

What Is Personal Budgeting?

Personal budgeting is the process of creating a plan for how you will spend, save, and manage your money over a specific period, usually monthly.

A budget helps you:

- Track income and expenses

- Avoid overspending

- Save for future goals

- Reduce financial stress

- Build healthy money habits

Think of a budget as a roadmap for your finances. Instead of wondering where your money went at the end of the month, you tell your money where it should go before you spend it.

Why Budgeting Is Important

Many people believe budgeting means restricting themselves or eliminating all enjoyment from life. In reality, budgeting provides freedom and clarity.

Benefits of budgeting include:

Better Financial Awareness

A budget shows exactly how much money you earn and where it goes.

Reduced Debt

Tracking spending helps identify areas where you can cut costs and use extra money to pay down debt.

Increased Savings

Budgeting encourages consistent saving habits, helping you build emergency funds and achieve long-term goals.

Less Financial Stress

Knowing your finances are organized can significantly reduce anxiety and uncertainty.

Improved Goal Achievement

Whether you want to travel, buy a home, start a business, or retire comfortably, budgeting helps make those goals achievable.

Understanding Your Financial Situation

Before creating a budget, you need a clear picture of your current financial position.

Start by gathering:

- Bank statements

- Credit card statements

- Loan information

- Pay stubs

- Utility bills

- Subscription records

Then calculate:

Total Monthly Income

Include all sources of income:

- Salary or wages

- Freelance work

- Side hustles

- Rental income

- Investment income

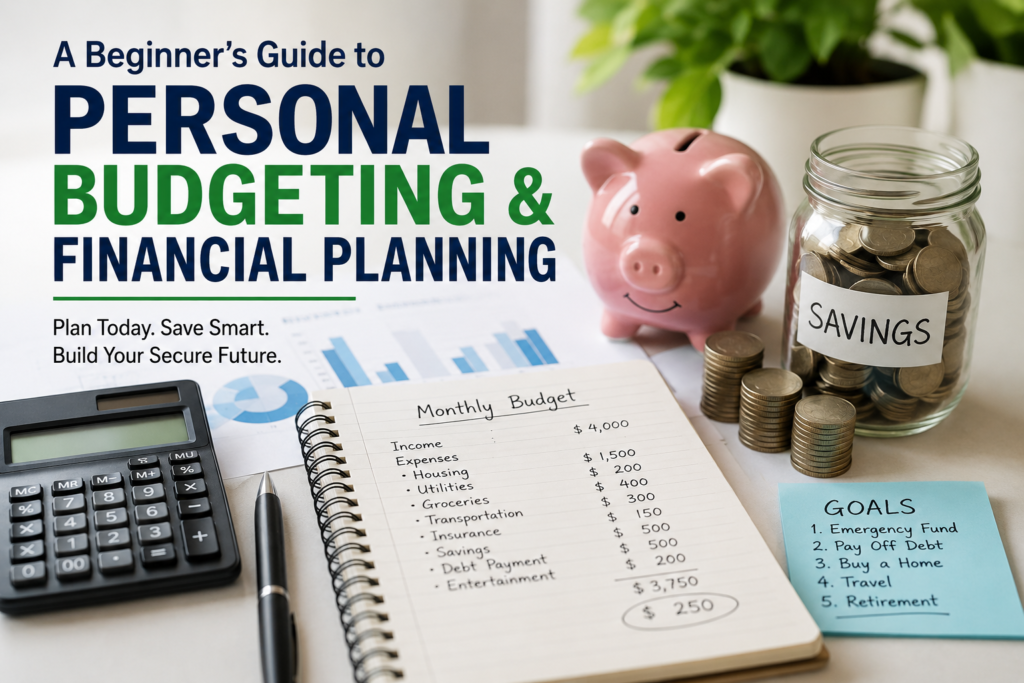

Example:

| Income Source | Monthly Amount |

|---|---|

| Salary | $3,500 |

| Freelance Work | $500 |

| Total Income | $4,000 |

Total Monthly Expenses

Categorize expenses into two groups:

Fixed Expenses

These remain relatively consistent each month.

Examples:

- Rent or mortgage

- Insurance

- Loan payments

- Internet service

Variable Expenses

These fluctuate monthly.

Examples:

- Groceries

- Entertainment

- Dining out

- Transportation

- Shopping

Once you’ve identified all expenses, compare them to your income.

Creating Your First Budget

The simplest way to begin is by using a budgeting framework.

The 50/30/20 Rule

One of the most popular budgeting methods divides after-tax income into three categories:

50% for Needs

Essential expenses such as:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

30% for Wants

Non-essential spending including:

- Streaming services

- Dining out

- Vacations

- Entertainment

20% for Savings and Debt Repayment

This portion goes toward:

- Emergency savings

- Investments

- Retirement contributions

- Extra debt payments

Example for a $4,000 monthly income:

| Category | Percentage | Amount |

|---|---|---|

| Needs | 50% | $2,000 |

| Wants | 30% | $1,200 |

| Savings/Debt | 20% | $800 |

This framework provides a balanced approach while remaining easy to follow.

Tracking Your Spending

Creating a budget is only the first step. You must also track your spending regularly.

Methods include:

Budgeting Apps

Popular budgeting tools can automatically categorize transactions and provide spending insights.

Spreadsheets

Many people prefer using Excel or Google Sheets for complete control.

Manual Tracking

Recording expenses in a notebook remains an effective option for those who prefer simplicity.

The key is consistency.

Even spending five minutes daily reviewing expenses can dramatically improve financial awareness.

Building an Emergency Fund

An emergency fund is one of the most important components of financial planning.

Unexpected expenses happen:

- Medical emergencies

- Job loss

- Car repairs

- Home maintenance

Without savings, these situations often lead to debt.

How Much Should You Save?

Financial experts generally recommend:

- Beginner Goal: $1,000

- Intermediate Goal: 3–6 months of expenses

- Advanced Goal: 6–12 months of expenses

Keep emergency funds in an easily accessible savings account.

The purpose is protection, not investment growth.

Managing and Eliminating Debt

Debt can be a major obstacle to financial freedom.

Common forms include:

- Credit card debt

- Personal loans

- Student loans

- Auto loans

The sooner debt is managed, the more money becomes available for savings and investments.

Debt Snowball Method

Focus on paying off the smallest balance first while making minimum payments on other debts.

Advantages:

- Quick wins

- Increased motivation

Debt Avalanche Method

Focus on debts with the highest interest rates first.

Advantages:

- Saves more money over time

- Reduces overall interest costs

Choose the approach that best fits your personality and financial situation.

Setting Financial Goals

A financial plan becomes much more effective when linked to clear goals.

Goals can be divided into three categories.

Short-Term Goals (0–2 Years)

Examples:

- Building an emergency fund

- Paying off credit card debt

- Saving for a vacation

Medium-Term Goals (2–10 Years)

Examples:

- Buying a car

- Starting a business

- Saving for a home down payment

Long-Term Goals (10+ Years)

Examples:

- Retirement planning

- Financial independence

- Funding children’s education

Use SMART goals:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Instead of saying:

“I want to save money.”

Say:

“I will save $5,000 for a home down payment within 18 months.”

Understanding Financial Planning

Budgeting focuses on day-to-day money management.

Financial planning focuses on your long-term financial future.

A comprehensive financial plan includes:

- Budgeting

- Saving

- Investing

- Insurance

- Retirement planning

- Tax planning

- Estate planning

Together, these components create a roadmap for lifelong financial stability.

The Importance of Saving

Saving should become a non-negotiable habit.

Many people wait until they have extra money left over each month.

Unfortunately, that rarely happens.

Instead:

Pay yourself first.

Automatically transfer money into savings as soon as income arrives.

Even small amounts accumulate over time.

For example:

- $5 per day = $1,825 annually

- $10 per day = $3,650 annually

Consistency matters more than size.

Introduction to Investing

Once you’ve established a budget and emergency fund, investing can help your money grow faster than traditional savings accounts.

Investing involves purchasing assets that may increase in value over time.

Common investment options include:

- Stocks

- Bonds

- Mutual funds

- Exchange-Traded Funds (ETFs)

- Real estate

Understanding Compound Growth

One of the most powerful concepts in finance is compound growth.

Money earns returns, and those returns generate additional returns.

A=P(1+nr)nt

PV

$

r

%

n

PV is starting amount; r is rate; n is number of periods.

FV=PV(1+r)n=1(1+0.05)20=2653.3dollars

The earlier you begin investing, the more time compound growth has to work in your favor.

Example:

- Invest $200 monthly at age 25

- Average annual return: 8%

- Continue until age 65

The result could exceed several hundred thousand dollars, depending on market performance.

Time is often more valuable than investment size.

Planning for Retirement

Retirement planning should begin as early as possible.

Many people underestimate how much money they will need later in life.

Retirement planning involves:

- Estimating future expenses

- Calculating retirement income needs

- Investing consistently

- Taking advantage of employer retirement programs when available

Starting early significantly reduces the amount needed each month to reach retirement goals.

Protecting Your Financial Future

Financial planning isn’t just about building wealth.

It’s also about protecting it.

Important types of insurance include:

Health Insurance

Protects against medical expenses.

Life Insurance

Provides financial support for dependents.

Disability Insurance

Replaces income if you’re unable to work.

Property Insurance

Protects homes, vehicles, and personal belongings.

Insurance acts as a financial safety net during unexpected events.

Common Budgeting Mistakes to Avoid

Many beginners encounter similar challenges.

Ignoring Small Expenses

Small purchases add up quickly.

Not Tracking Spending

A budget without tracking is ineffective.

Setting Unrealistic Goals

Overly strict budgets often fail.

Forgetting Irregular Expenses

Plan for annual expenses such as:

- Insurance renewals

- Vehicle maintenance

- Holiday spending

Giving Up After Mistakes

Budgeting is a skill that improves with practice.

One bad month doesn’t mean failure.

Simple Financial Habits That Build Wealth

Long-term financial success often comes from small daily actions.

Develop habits such as:

- Spending less than you earn

- Saving consistently

- Avoiding unnecessary debt

- Reviewing finances monthly

- Investing regularly

- Continuing financial education

Over time, these habits create significant results.

A Beginner’s 30-Day Financial Action Plan

Week 1

- Calculate monthly income

- Track all expenses

- List debts

Week 2

- Create a realistic budget

- Cancel unnecessary subscriptions

- Open a savings account if needed

Week 3

- Set three financial goals

- Begin building an emergency fund

- Automate savings transfers

Week 4

- Review spending patterns

- Adjust your budget

- Learn basic investing concepts

After 30 days, you’ll have greater financial clarity and a strong foundation for future growth.

Final Thoughts

Personal budgeting and financial planning are not about becoming wealthy overnight. They are about making intentional decisions with your money so you can create financial stability, reduce stress, and achieve meaningful life goals.

The journey begins with understanding your income, tracking expenses, creating a realistic budget, and building healthy financial habits. As your confidence grows, you can expand into saving, investing, retirement planning, and long-term wealth building.

Remember that financial success is rarely the result of a single decision. It is the outcome of consistent, disciplined actions repeated over time. Start small, stay committed, and allow your financial plan to evolve as your life and goals change.

The best time to take control of your finances was years ago. The second-best time is today.